Explanatory Notes on Main Statistical Indicators

Industry

refers to the material production sector

which is engaged in extraction of natural resources and processing and

reprocessing of minerals and agricultural products, including: (1) extraction

of natural resources, such as mining, salt production (but not including

hunting and fishing); (2) processing and reprocessing of farm and sideline

produces, such as rice husking, flour milling, wine making, oil pressing, silk

reeling, spinning and weaving, and leather making; (3) manufacture of

industrial products, such as steel making, iron smelting, chemicals

manufacturing, petroleum processing, machine building, timber processing; water

and gas production and electricity generation and supply; (4) repairing of

industrial products such as repairing of machinery and means of transport

(including cars).

Prior to 1984, the rural industry run by

villages and cooperative organizations under village was classified into

agriculture. Since 1984, it has been grouped into industry. Units of industrial

statistics survey corporate industrial enterprises with independent accounting

system.

Corporate industrial enterprises with

independent accounting system refer to enterprises engaging in industrial

production activities, which meet the following requirements: they are

established legally, having their own names, organizations, location, able to

take civil liability; they possess and use their assets independently, assume

liabilities, and are entitled to sign contracts with other units; they are

financially independent and compile their own balance sheets.

Light

Industry

refers to the industry that produces consumer goods and hand tools. It

consists of two categories, depending on the materials used: (1) Industries

using farm products as raw materials. These are branches of light industry

which directly or indirectly use farm products as basic raw materials,

including the manufacture of food and beverages, tobacco processing, textile,

clothing, fur and leather manufacturing, paper making, printing, etc. (2)

Industries using non farm products as raw materials. These are branches of

light industry which use manufactured goods as raw materials, including the

manufacture of cultural, educational articles and sports goods, chemicals,

synthetic fiber, chemical products for daily use, glass products for daily use,

metal products for daily use, hand tools, medical apparatus and instruments,

and the manufacture of cultural and clerical machinery.

Heavy

Industry

refers to the industry which produces capital goods, and provides various

sectors of the national economy with necessary material and technical basis. It

consists of the following three branches according to the purpose of production

or the use of products: (1) Mining, quarrying and logging industry refers to

the industry that extracts natural resources, including extraction of

petroleum, coal, metal and non-metal ores. (2) Raw materials industry refers to

the industry that provides various sectors of the national economy with raw

materials, fuels and power. It includes smelting and processing of metals,

coking and coke chemistry, chemical materials and building materials such as

cement, plywood, and power, petroleum refining and coal dressing. (3)

Manufacturing industry refers to the industry that processes raw materials. It

includes machine building industry which equips sectors of the national

economy, industries of metal structure and cement products, industries

producing means of agricultural production, such as chemical fertilizers and

pesticides. According to the above principle of classification, the repairing

trades which are engaged primarily in repairing products of heavy industry are

classified into heavy industry while these engaged in repairing products of

light industry are classified into light industry.

Industrial

Enterprises above Designated Size

refer to industrial enterprises as legal person with annual business

revenue of over 20 million yuan.

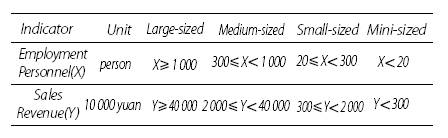

Large,

Medium, Small, Mini-sized Enterprises

Industrial enterprises are classified into

large, medium, small, mini-sized enterprises according to employment personnel

and sales revenue in accordance with the regulation of Classification of Large,

Medium, Small, Mini-sized Enterprises on Statistics in 2011. The standard of

classification as following:

Gross

Output Value of Industry��current price��

refers to total volume of final industrial products produced and

industrial services provided during the reporting period. It consists of 3

components: value of the finished products, income from processing for external

parties, and value of change in semi-finished products between the end and the

beginning of the reference period.

Total

Assets

refer to all resources formed by transaction or other activities, which

are owned or controlled by enterprises and expected to bring economic benefits

to the enterprises. Classified by the degree of liquidity(the

time of assets to be liquidated or consumed), total assets include working

capitals and immovable assets. Working capitals can be classified into monetary

assets, trading financial assets, notes receivable, accounts receivable,

advanced payments, other prepaid money and inventories. Immovable assets can be

divided into long-term equity investment, fixed assets, intangible assets and

other immovable assets.

Working

Capitals

the assets should be classified into working

capital if meeting one of the following conditions: (1) expected to be

liquidated, sold or consumed in one normal operating cycle, mainly including

inventory, account receivable, etc.; (2) owned for transaction purpose; (3)

expected to be liquidated in one year (including one year) since balance sheet

date; (4) cash or cash equivalent without limited ability of exchanging other

assets or paying debts in one year from balance sheet date, including monetary

funds, note receivable, accounts receivable, inventory and other items.

Fixed

Assets

refer to the physical assets owned over one

accounting year for the purpose of production, providing services, rent or

business management, including the use of more than one year of housing,

buildings, machines, machinery, transport equipment and other production and

business-related equipment, apparatus, tools, etc.

Revenue

from Principal Business

refers to revenues accepted by enterprises from the sales of products, labour services provided and etc. in the principal

business.

Cost

of Principal Business

refers to total costs for enterprises to operate the principal business.

Tax

and Extra Charges of Principal Business

refer to the tax and charges including the business tax, consumption tax,

city maintenance and construction tax, resources tax, land increasing value tax

and extra charges for education and etc. in the operation of principal

business.

Total

Pre-tax Profits

refer to the business results of enterprises in certain accounting

period, that is the profits gained from the revenues after deducting the costs,

which means the final achievements in the reference period. To the enterprises

implemented the Regulation of Accounting Standards for Business Enterprises in

2006, total pre-tax profits equals to business profit add non-operating revenue

and minus non-operating expenditures. To the enterprises not implemented, total

pre-tax profits equals to business profit add investment income, subsidies,

non-operating revenue and minus non-operating expenditures.

Total

Profits and Taxes

refers to the sum of the total profits, tax and extra charges of principal

business and the value added tax payable of industrial enterprises.

Proportion

of Products Sold

reflects the actual sale of industrial products, analyzing the

production-selling and supply-demand relations. It is calculated as:

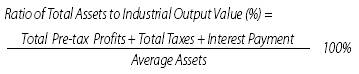

Ratio

of Total Assets to Industrial Output Value

reflects the profit-making capability of all assets of the enterprise and is

a key indicator manifesting the performance and management and evaluating the

profit-making potential of the enterprise. It is calculated as follows:

In the above formula, total taxes is the sum

of tax and extra charges of principal business and value-added tax payable; and

average assets is the arithmetic mean of the sum of beginning assets and ending

assets.

Ratio

of Debts to Assets

reflects both the operation risk and the capability of the enterprise in

making use of the capital from the creditors. It is calculated as follows:

![]()

Number

of Times of Turnover of Working Capitals

refers to the number of times of turnover of working capital in a given

period of time, which reflects the speed of the turnover of working capital of

industrial enterprises, and is calculated as follows:

In the above formula, average balance of

total working capital refers to the arithmetic mean of the sum of circulating

funds at the beginning and at the end of the reference period.

Ratio

of Pre-tax Profits to Total Industrial Costs

refers to the ratio of profits realized in a given period to the total

costs in the same period, which reflects the economic efficiency of input cost

and is calculated as follows:

Total costs in the above

formula is the sum of cost of products sold,

marketing cost, management cost and financial cost.

Liquidity

Ratio

refers to the ratio of current assets and current liabilities, which is

used to measure the enterprise's ability to turn the current assets into cash

to repay its debts before the short-term debt maturity. It is calculated as

follows:

![]()

Quick

Ratio

refers to the ratio of quick assets and current liabilities, which is used

to measure the enterprise��s ability to turn the current assets into cash

immediately to repay its current liabilities. It is calculated as follows:

![]()